Is there a bullish IBEX35?

For 2021, high quality assets in Spain seem like a good opportunity.

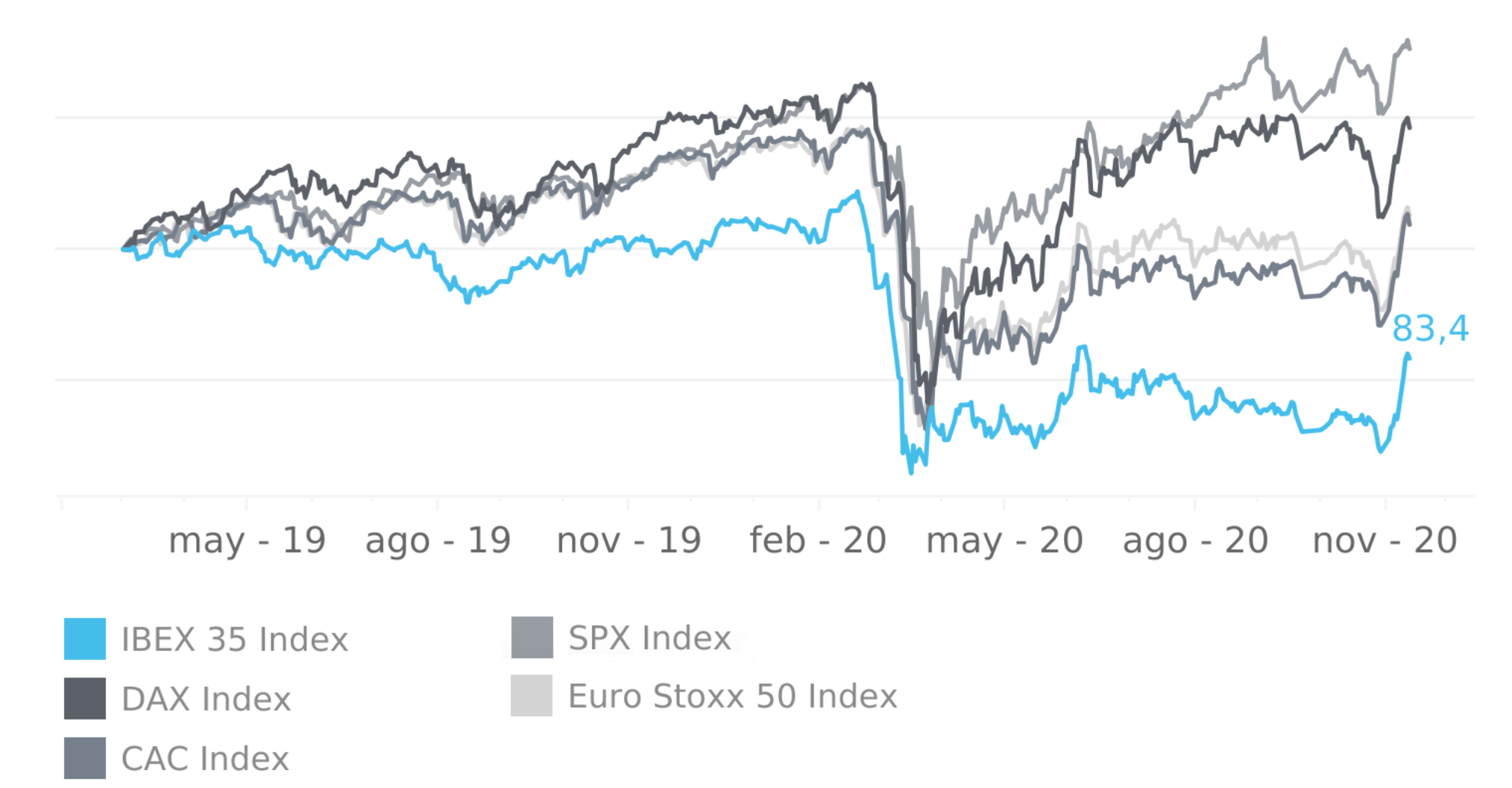

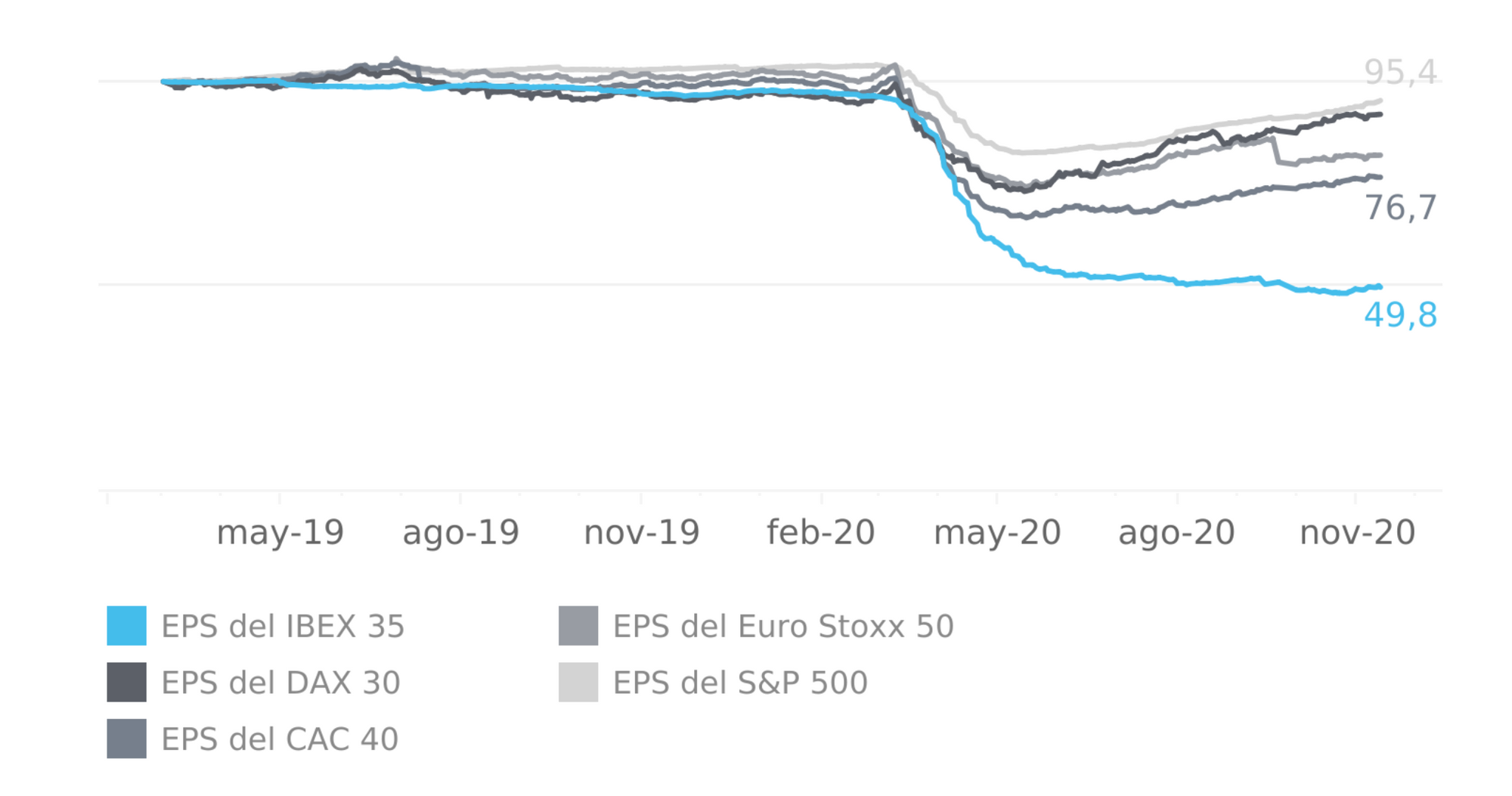

Think for simplicity that rather than having a big number of investors we have one deep pocket investor. She would build a market portfolio holding both bonds and equities. Routinely scanning for new opportunities and higher earnings she visits the financial information in 360smartvision.com and observes that since March 2019 the S&P 500 index shows higher performance than its European counterparts. The flow of capital mainly allocated to technological stocks increased in 2019 and in the aftermath of the April 2020 COVID recovery. By contrast the blue line in Figure 1 shows that the IBEX 35 has been the worse performing index in Europe. As depicted in Figure 2 earnings per share (EPS) have been low in Europe and specially in Spain. As a result they were poorly weighted in the investors portfolio. That brought high evaluations in the US markets in the 2019-2020 period.

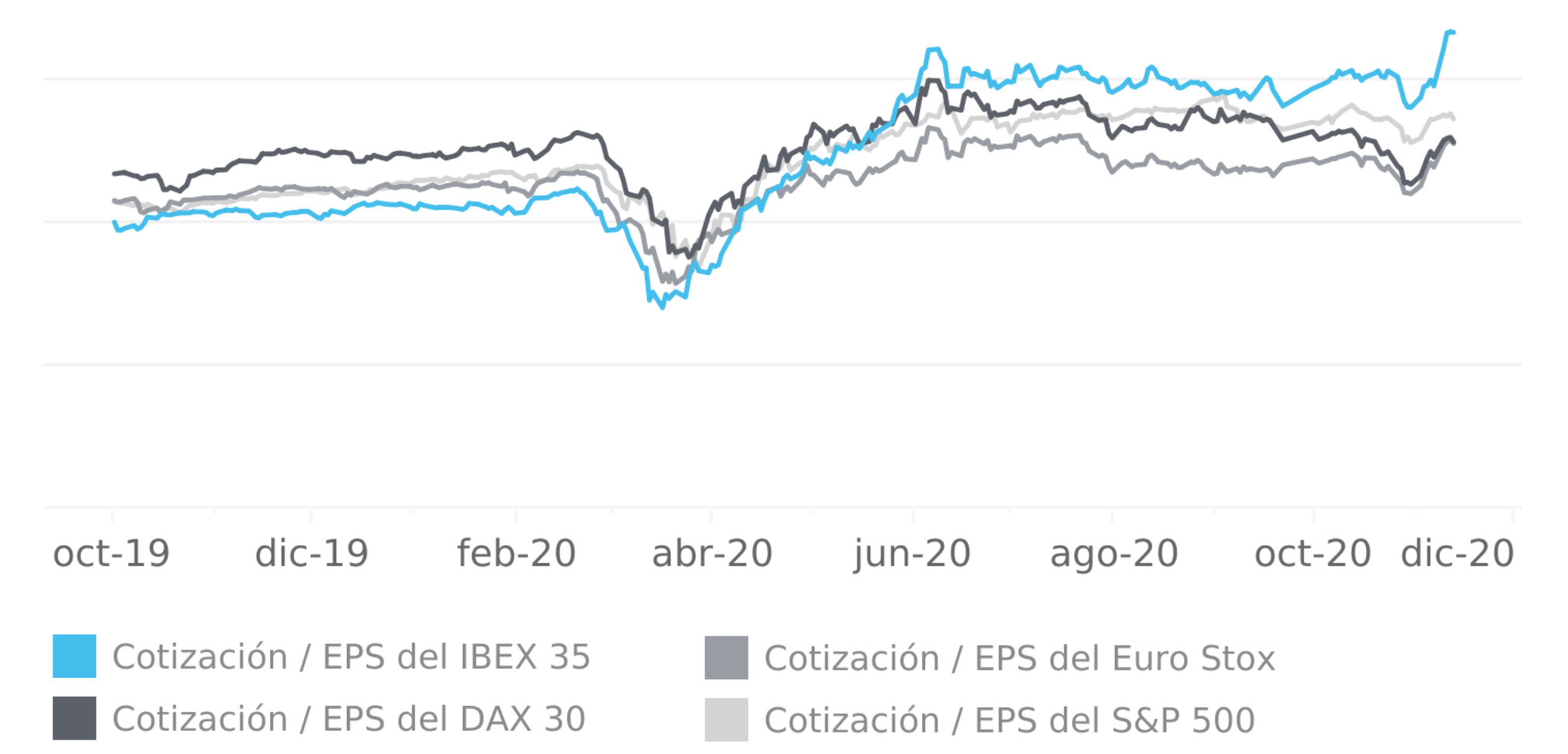

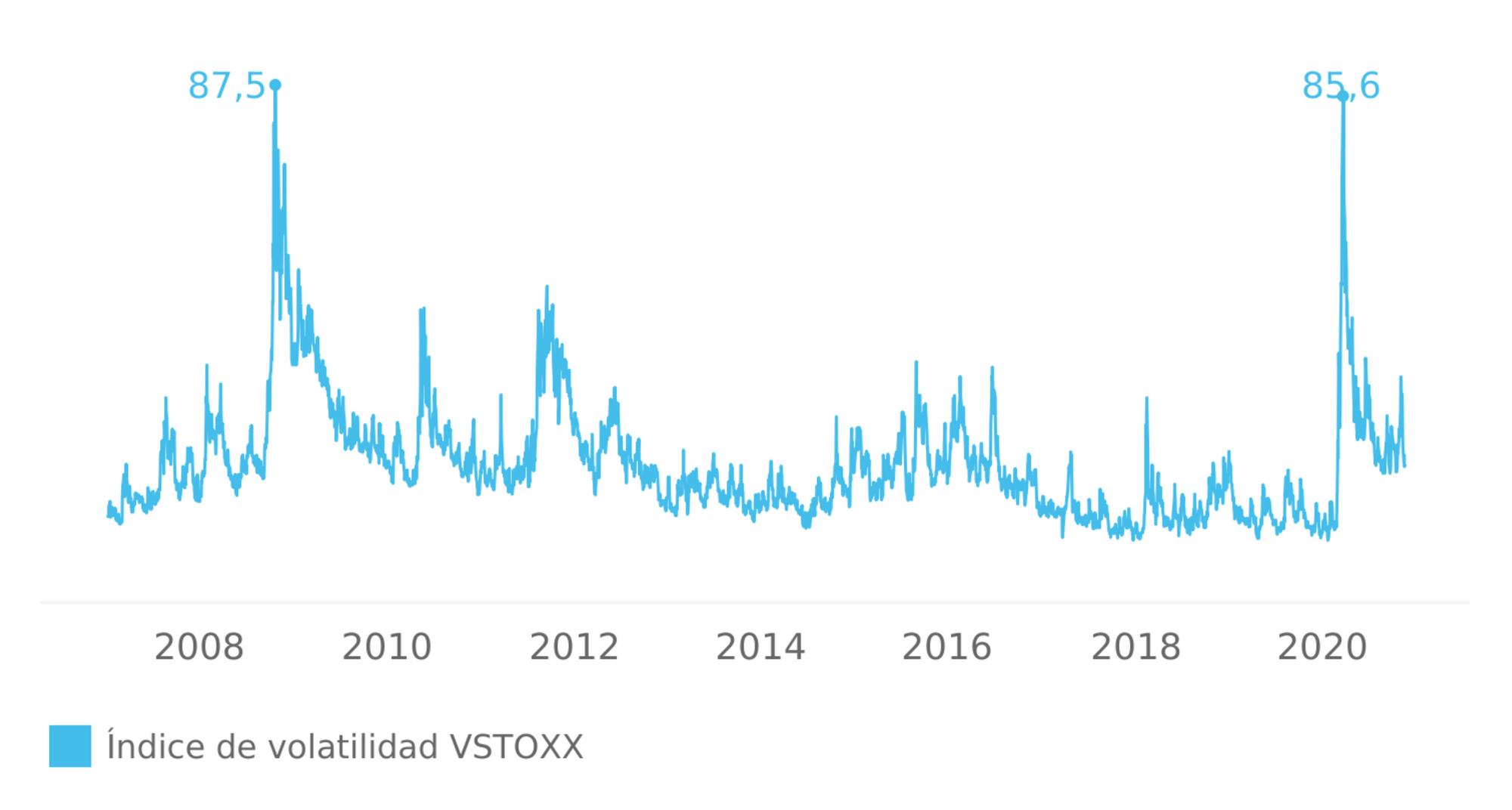

However a close look to Figure 3 shows that price earnings ratios are highest for the IBEX-35 when compared to the American benchmark and the European counterparts. This implies that equity prices are trading far from fundamental values in the Spanish market and this pattern has inten- sified over the past month. The main question that we ask is whether this reflects bubble like behaviour or investor expectations of future corporate fundamental growth. For 2021, high quality assets in Spain seem like a good opportunity as the deep pocket investor would seek spreading the risk taking by considering higher weighting of European stocks in her portfolio. Indeed the forward looking volatility in Europe has reached 23%, trading within the lowest level range seen since the COVID outbreak (see Figure 4). Furthermore the volatility spread between VIX and VSTOXX, is hovering 0.31 percentage points higher in the US than in Europe since April 2020. That reflects that Europe is coming out strong from the COVID 19 virus attack and would also profit from the positive news related to the reliability of newly tested COVID 19 vaccines.

The change of the American administration is expected to restore relationships with Europe and drop trade tariffs. Member states are well oiled from common funds available to rebuild and transform the local economies too. The deep pocket investor would exploit those positive expectations by allocating more capital in Europe. We believe that the trend of very low earnings reported for Spanish corporates is about to change, as earnings expectations are getting steeper, for the deep pocket investor. The Spanish collateral of growth comes from strong recovery in the manufacturing sector (see the PMI manufacturing reaching 52.5 in October), good infrastructure state, with strong investment renewable sources of power generation, lower maintenance bills than most western countries, extended fibra coverage, rapid 5G deployment, and major data hub development to pursue the coming digital transformation. These are good news that push down the 10 year credit spreads (see Figure 5), and facilitate a fiscal expansion of historic proportions. We therefore can state that the Ibex 35 is looking bullish.